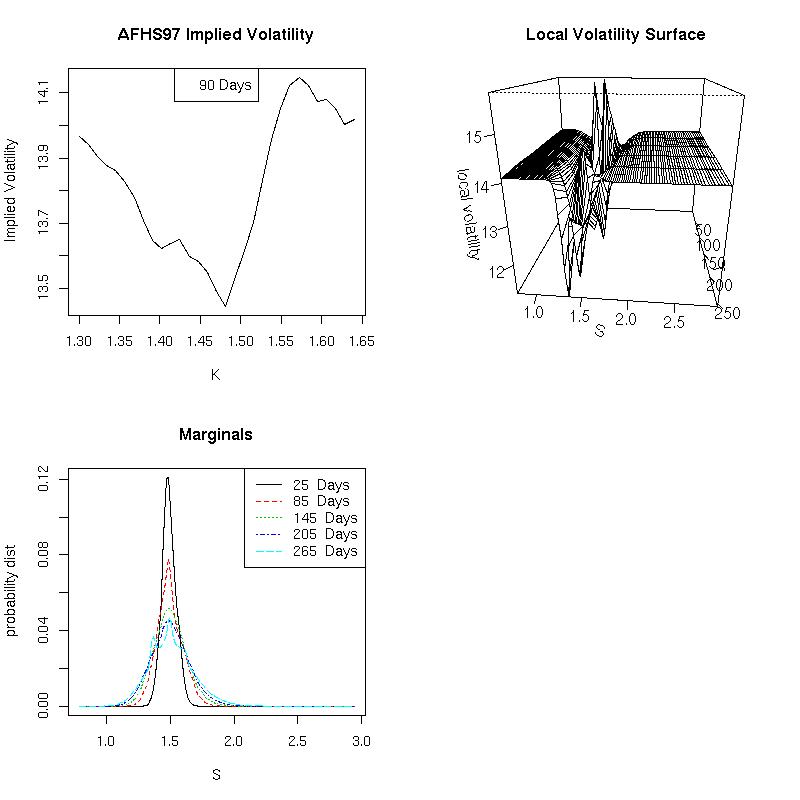

Calibrates a diffusion pricing model using the methodology and data of

Avellaneda, Friedman, Holmes, Samperi (1997), or AFHS97,

and displays 90-day implied volatilities, along with the implied local

volatility surface and the marginals (computed via forward induction).